FAQ

-

Show Hide

Do we need to have an additional agreement for our direct debits?

This depends on the processing bank that is used in the background. If you continue to offer direct debits in the same countries, then no additional agreements are required.

-

Show Hide

Do you generate a mandate that we can use to send to our customer or do we need to build the mandate ourselves?

The GlobalCollect platform generates an unique mandate reference and informs you when you request the information related to the token, which you should include in the mandate that is sent to a customer. You will remain responsible for the mandate process. A consumer should sign the mandate and send it back to you. In principle, you should validate the token as soon as you receive the signed mandate back from the consumer.

-

Show Hide

Can we capture a mandate online, real-time on a screen?

There is no official SEPA electronic mandate yet but based on the feedback received from other merchants to date, some are looking into developing the “I Accept” functionality that would be used as the consumer’s confirmation. As it is not a SEPA approved process to capture mandates, the merchants that implement an alternative to the paper mandate would need to consider the risk of consumer payment reversals up to 13 months after the payment was collected. As soon as SEPA goes “live”, 13 months will apply to all SEPA countries. The first step in the process is to create token. Upon the receipt of the successful response the information of the token should be requested. In the response the mandate ID and other details (our creditor ID) will be provided. These details should be included on the mandate. As soon as a consumer signs the mandate and returns it, a validation of a token can be done and an new payment can be submitted. The mandate reference will be submitted to the bank of the consumer by us with the payment request. The consumer will be able to link the mandate reference on a bank statement for an individual charge with the mandate reference as provided on a mandate.

-

Show Hide

Can you send the pre-notification to our customers?

We have the option to send a pre-notification to the customer. Please look at the SEPA page for more information.

-

Show Hide

Do I need a paper mandate?

The obligation to manage mandates remains with you, and no electronic equivalent has been accepted as an official debit mandate, therefore we recommend that you still maintain paper mandates. You will need to confirm the validation of the token to us after you have obtained a mandate from the consumer. Transactions will not be rejected by us or the banks if there is no paper mandate.

-

Show Hide

Can SEPA Direct Debit mandates expire?

Yes, a mandate will expire after 36 months if it is not used.

-

Show Hide

Are we required to validate the token to be able to collect funds from a customer's bank account?

A validation of the token is required, which can be done immediately after the mandate process is completed. Example: If you present a mandate to a consumer in a similar way as acceptance of terms and conditions, you can validate the token immediately after a consumer confirms the agreement to debit his account online. Validation is a pre-requisite to proceed with the payment process.

-

Show Hide

Are we required to send the collected mandates?

You are responsible for managing mandates. You do not have to send the collected mandates to us confirming the signed mandate is required. You should store the mandates on your end for any future inquiries from the banks.

-

Show Hide

How should SEPA Direct Debit mandates be stored? And for how long?

If a paper based mandate is captured, the documents have to be dematerialized. This means that they have to be scanned and stored. You are free to choose their own method of storing digital data.

-

Show Hide

How can I validate the IBAN and BIC?

Bank account validation option will allow you to validate the submitted details in IBAN or BBAN format.

-

Show Hide

For the validation and collection process, do we keep the same Payment Product ID we already use?

For SEPA Direct Debits we use one payment product ID (770) for all direct debit countries. The country code in the request will differentiate between the countries.

-

Show Hide

Does SCT or SDD enable the simple validation of a transaction when money collection is done by our customer?

The bank validation option will stay the same – we will be using the same solution and validation will be done based on the IBAN and BIC that will be submitted in the validation requests by you. You can choose to use the bank account validation option. With this option you can validate the following data: only BBAN, only IBAN or both IBAN and BBAN (these must match).

-

Show Hide

For SEPA Direct Debit will only one bank account be used or will we still use the local bank accounts?

Currently the GlobalCollect platform offers a wide range of local channels to process payments with parties that are known and trusted by consumers. With SEPA, we will continue to process via local channels until consumers become accustomed to transacting with bank accounts anywhere in the SEPA region.

-

Show Hide

Do you provide a convertor from BBAN to BIC and IBAN?

Conversion can be done by batch or on an individual order basis. Please contact Implementation Support for details.

-

Show Hide

Do you provide mandate templates in all the languages of the SEPA countries?

Yes, in offline versions.

-

Show Hide

Do you provide local addresses (P.O. Box) for the return of the signed mandates?

Currently this is not offered, the mandate has to be returned to you.

-

Show Hide

What does my company need to do to be ready for SEPA Direct Debit?

You need to integrate the new Payment Product ID's and related API's. If you have legacy mandates then the implementation team should be contacted for assistance in migrating these transactions.

-

Show Hide

What does Worldline SEPA compliancy mean to me?

Because we are SEPA compliant, it is currently capable of supporting the required formats for the payment products it offers in SEPA countries. This varies from local formats for direct debits to providing the required bank details for credit transfers.

-

Show Hide

What is an IBAN?

The IBAN is the International Bank Account Number. It is an internationally agreed format for the BBAN and includes the ISO country code and two check digits. In 2001 the decision was made to make IBAN the standard bank account format within the SEPA region. Outside the SEPA zone, an increasing number of countries are using the IBAN format.

-

Show Hide

What is a BIC?

The BIC is the Business Identifier Code, also known as SWIFT or Bank Identifier code. It is a code with an internationally agreed format to Identify a specific bank. The BIC contains 8 or 11 positions: the first 4 contain the bank code, followed by the country code and location code.

-

Show Hide

What is a Unique Mandate Reference?

For each direct debit mandate a Unique Mandate Reference has to be created. This number has to be unique for each Creditor Identifier and therefore is created by GlobalCollect.

-

Show Hide

What is a BBAN?

The BBAN is the Basic Bank Account Number. The BBAN format is decided by each national banking community under the restriction that it must be of a fixed length of case-insensitive alphanumeric characters. It includes the domestic bank account number, branch identifier, and potential routing information.

-

Show Hide

What is a Creditor Identifier?

The Creditor Identifier is a unique code and is assigned to the company that is listed as the creditor. We will be listed as the creditor and our Creditor Identifier will be used to process direct debits. The Creditor Identifier will be reported to the consumer for each direct debit processed.

-

Show Hide

What are the benefits of SEPA?

The SEPA initiative can be seen as the next phase of a process to simplify the payment landscape between European countries. The first phase was achieved with the creation a single currency that can be used in several countries: the EURO. This change has made it easier to process transactions between member states, but there were still localized systems to facilitate these payments. SEPA was designed to create a single payment format between all member states and to make transactions within the SEPA zone as easy as the current domestic payments system.

-

Show Hide

What are Legacy Direct Debits?

Legacy Direct Debits represent all the direct debit flow that currently is processed under the domestic Direct schemes and will be processed under the same conditions (apart from the new payment details required for a transaction) in the SEPA Direct Debit format. Legacy direct debits are treated differently when it comes to obtaining a mandate. No new mandate has to be obtained before a direct debit can be processed.

-

Show Hide

What is SEPA?

SEPA (Single EURO Payment Area) is a European regulatory initiative to create a standard format for processing transactions across 33 markets in Europe. Compliance to the SEPA format is a mandated requirement. For EURO countries within SEPA, the compliance deadline is 1 February, 2014. This date was extended until 1 August, 2014. For non-EURO countries within SEPA, the compliance deadline is 1 February, 2016. In non-EURO countries Credit Transfer and Direct Debit products will still be available in the domestic format after February 1, 2014.

2014

Austria

Austria Belgium

Belgium Cyprus

Cyprus Estonia

Estonia Finland

Finland France

France Germany

Germany Greece

Greece Ireland

Ireland Italy

Italy Luxembourg

Luxembourg Malta

Malta Monaco

Monaco The Netherlands

The Netherlands Portugal

Portugal Slovakia

Slovakia Slovenia

Slovenia Spain

Spain

2016

Bulgaria

Bulgaria Croatia

Croatia Czech Republic

Czech Republic Denmark

Denmark Hungary

Hungary Iceland

Iceland Latvia

Latvia Liechtenstein

Liechtenstein Lithuania

Lithuania Norway

Norway Poland

Poland Romania

Romania Sweden

Sweden Switzerland

Switzerland United Kingdom

United Kingdom

-

Show Hide

What will happen if we do not receive the signed mandates in time for the February collections? Is there any grace period?

There are three scenario's:

- If you have a legacy order and has captured a mandate: you can continue to process and do not have to register a new mandate.

- If you have a legacy orders and never captured a mandate: The mandate must be collected and the transaction can only be processed once the mandate is returned.

- If you submit a new SEPA Direct Debit transaction prior to February 1st: The mandate must be collected and the transaction can only be processed once the mandate is returned.

-

Show Hide

What types of rejection are possible?

See Error code Guide for information on rejections.

-

Show Hide

What is pre-notification and how must it be communicated?

Pre-notification is a message to the customer that provides details about the direct debit. This includes information about the order, the amount, frequency and date. In addition, information such as the Unique Mandate Reference and Creditor ID associated with the transaction, must be included.

-

Show Hide

What is the difference between SEPA Direct Debits Core and B2B?

SEPA Direct Debit Core is designed for business-to-consumer transactions, but via this scheme it is possible to process business-to-business transactions as well. In the B2B direct debit scheme only business-to-business accounts can be processed, and transactions from consumer accounts will fail. We will only offer the SEPA Direct Debit Core scheme, which will allow you to process direct debits from both consumer and business accounts. The main difference from a mandate perspective is that with SEPA Direct Debit Core scheme the you are responsible for capturing a mandate, while with B2B Direct Debits the party that is being debited is responsible for registering the mandate with the bank.

-

Show Hide

Will there be any differences for variable recurring transactions in SEPA?

No. For the first transaction, a new mandate reference will be registered and the same mandate reference will be assigned to all subsequent recurring transactions.

-

Show Hide

Will there be changes in reporting from the GlobalCollect platform?

The structure of the reports will not change. Please be advised that the SEPA Direct Debit scheme will introduce a couple of new reversal reasons. These reasons will be reported in the daily report files.

-

Show Hide

Why do we need SEPA?

SEPA is a mandatory change amongst participating countries. It will introduce a uniform payment processing format, but changes are required to comply with the new standards.

-

Show Hide

If the name of the creditor in the mandate is GlobalCollect, how can the consumer identify that you collect the funds on behalf of our company?

You are able to submit a soft descriptor in the direct debit text field. This will help the customer to recognize the transaction.

-

Show Hide

Is a new contract needed if we migrate to SEPA Direct Debit?

No, the contract remains unchanged.

-

Show Hide

How will recurring transactions work (multiple transactions per mandate)?

For the first transaction, a new mandate reference will be created and the same mandate reference will be assigned to all subsequent recurring transactions.

-

Show Hide

How will one-off transactions work in SEPA?

For each one-off transaction, a unique single use mandate reference will be created.

-

Show Hide

Where will I get my customers' IBAN and BIC?

The IBAN and BIC from the customer will need to be captured during the transaction. If only the BBAN details are captured, then we can assist with the conversion to IBAN.

-

Show Hide

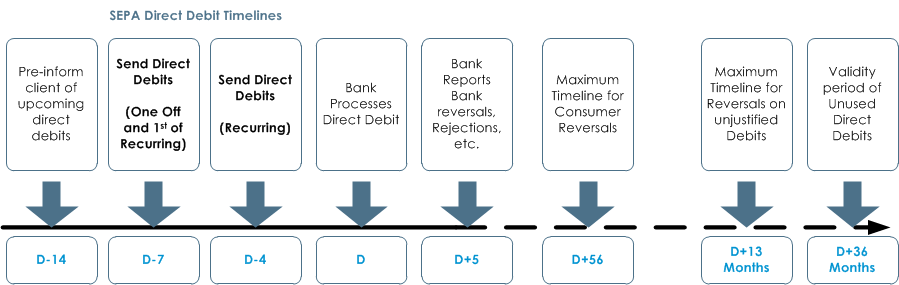

What are the timelines for SDD processing?

The direct debit has to be provided to the bank 2 days prior to the value date. This means that you either have to plan direct debit batches ahead, in order to be able to debit customers at a certain time, or have to be aware that the direct debit process will take longer to complete.

If you are processing direct debits on a variable recurring bases are advised to process the direct debits as recurring instead of one-off.

Within 5 working days after the value date, bank reversals (refusals, rejections, etc.) will be reported by the processing banks.

Within 56 working days after the value date, consumers can reverse their transaction without providing further explanation to their bank.

Within 13 months after the value date, consumers can reverse any unjustified direct debits.

In case a mandate is not used for 36 months it will no longer be valid and a new mandate will need to be signed.

Please find below schematic overview of the SEPA Direct Debit timelines:

Please note that this is a standard timeline. On an individual processing bank basis there could be slight deviations from this model.

Please note that this is a standard timeline. On an individual processing bank basis there could be slight deviations from this model.Example 1

In case you want to debit the consumer on the 10th day of the month, the direct debit will need to be instructed at least 1 working days prior to this date. Bearing in mind the processing date in the system, the order needs to be submitted 2 days prior to the value date.

Example 2

In case you want to debit the consumer as quickly as possible . The direct debit will take 2 working days before the bank processes the direct debit.

-

Show Hide

We never collected mandates, how do we migrate our Direct Debit?

Transactions without mandates (electronic and paper) need to be treated as new transactions.

-

Show Hide

If there is no signed mandate in place, could we expect the customer to demand a reversal for up to 13 months? Is that without any questions asked, even though the customer has received the goods or services?

If you are not able to present a signed, paper mandate, a consumer has the right to reverse the payment. Worldline therefore recommends that you comply with the paper mandate requirement. Too many reversed payments due to lack of mandate may damage relationships with the banks.

-

Show Hide

Is it still possible for us to generate our own order IDs with SEPA Direct Debit?

No, order IDs will be generated by us. You should store tokens for recurring requests. The GlobalCollect platform introduced a field where your own order ID can be inserted when submitting a new transaction.

-

Show Hide

What affect will SEPA have on our customers?

Customers will be introduced to a new standard for payment processing. The customer’s bank will have to instruct customers about this change and it will most likely take some time to be adopted.

-

Show Hide

We don't have offices in Europe. What will SEPA mean for us?

If you do not have an office in Europe, but use GlobalCollect's services to process bank transfers, bank refunds, payouts or direct debits in one of the EURO countries, then you have to implement the changes related to SEPA.

-

Show Hide

Is the IBAN enough to process money collection requests? Or will BIC also be needed?

The BIC is an optional field for SEPA Direct Debit (PPID 770) and SEPA Credit Transfers (PPID's 11, 1070, 1270). In terms of banking details the IBAN will be sufficient to process a transaction.

-

Show Hide

Are card payments affected by SEPA?

No, SEPA only affects Credit Transfer and Direct Debit products. In the first phase EURO countries will be migrated on February 1st, 2014. In a later phase non-EURO member countries will be migrated.

-

Show Hide

Are EURO payments outside SEPA affected?

This depends on the country of the bank account to which the funds will be transferred. If the country is within the SEPA zone, the IBAN always has to be used.